Forensic Accounting · Numerawise Solutions

What Is Forensic Accounting? What Does a Forensic Accountant Do?

Forensic accounting is the disciplined use of accounting knowledge and investigation to find out what truly happened in a set of financial records. This guide explains what a forensic accountant does, when your business needs one, and how Numerawise supports your CPA or attorney.

Key takeaways

- Forensic accounting investigates a specific concern in your financial records — such as fraud, theft, missing money, or a partner dispute.

- Numerawise provides forensic bookkeeping support: data reconstruction, transaction tracing, and clear schedules. Your own licensed CPA provides any formal opinion or testimony.

- Common triggers include balances that won’t reconcile, withheld records, unexplained payroll, or preparing for litigation, a buyout, or an insurance claim.

- Every engagement starts with a free scoping call and a fixed-price scope where possible.

The basics

What Is Forensic Accounting?

Forensic accounting is the disciplined use of accounting knowledge and investigative technique to determine what truly occurred within a set of financial records. It is most often called upon when a business owner suspects fraud, theft or hidden income — or when financial records must withstand scrutiny by a licensed CPA, an attorney, an insurer or a court.

At Numerawise Solutions we provide forensic bookkeeping support, financial data reconstruction and transaction analysis. We are not a CPA firm and we do not provide audits, attest services, legal advice, formal forensic opinions or court testimony. When findings must carry a formal opinion or be presented in a legal proceeding, that responsibility rests with the client’s own licensed CPA, CFE or attorney.

The work

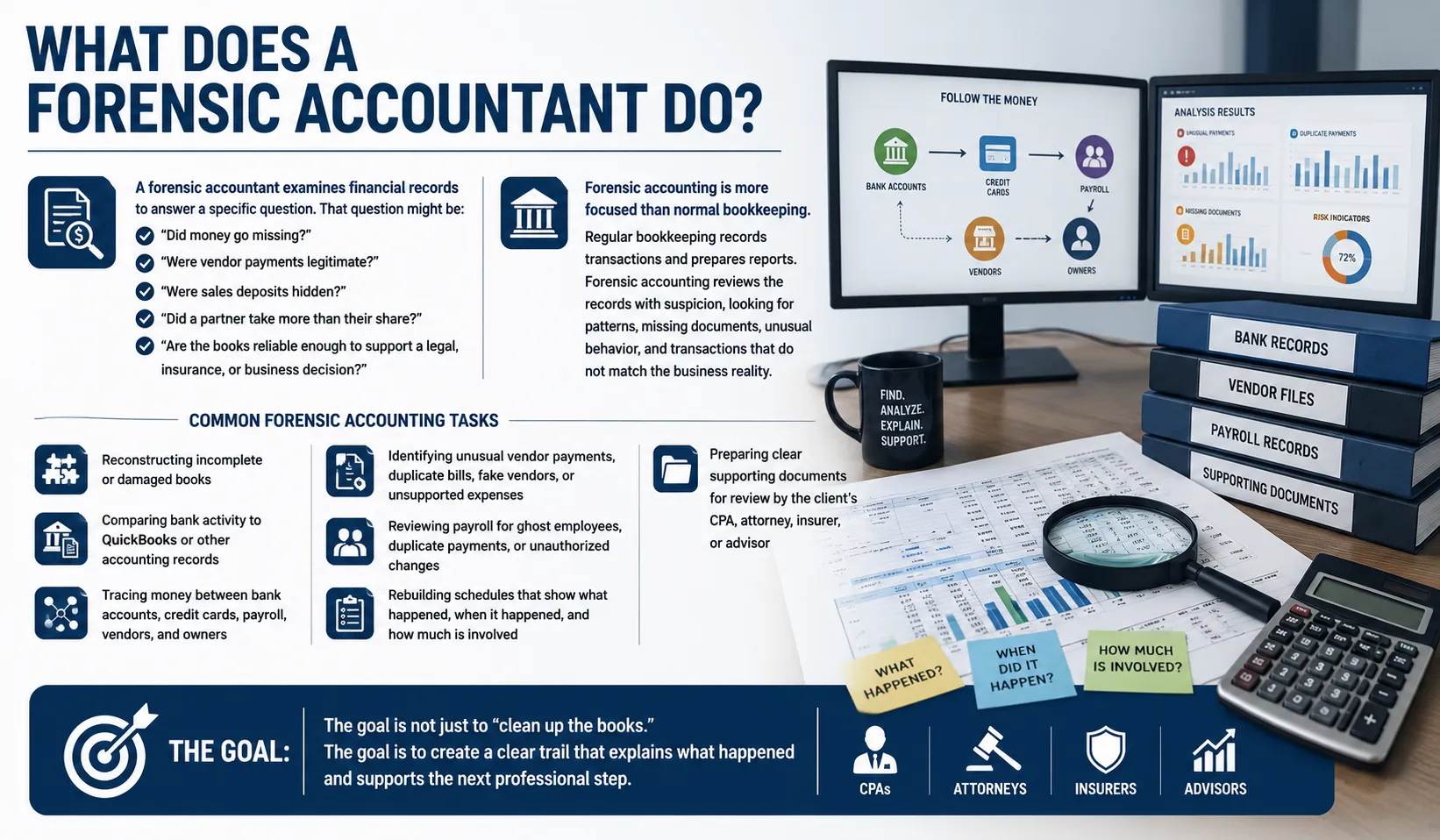

What Does a Forensic Accountant Do?

A forensic accountant examines financial records to answer a precise question. That question may take many forms:

Forensic accounting is considerably more focused than ordinary bookkeeping. Standard bookkeeping records transactions and prepares financial reports with the working assumption that the underlying records are honest. Forensic accounting approaches those same records with professional skepticism — looking for patterns that do not fit, documents that are absent, behavior that is inconsistent and transactions that contradict the economic reality of the business.

Common tasks in a forensic engagement include reconstructing incomplete or damaged records, comparing bank activity to QuickBooks or other accounting software, tracing the movement of funds across bank accounts and payroll systems, identifying fictitious vendors or duplicate billing and preparing clear transaction schedules that the client’s CPA or attorney can review and act upon.

The objective is never simply to tidy the books. The objective is to establish a clear financial trail that explains what happened and equips the next qualified professional to take appropriate action.

Not sure if you need a forensic review?

Start with a free, no-obligation scoping call. We’ll tell you honestly what’s needed.

Know the difference

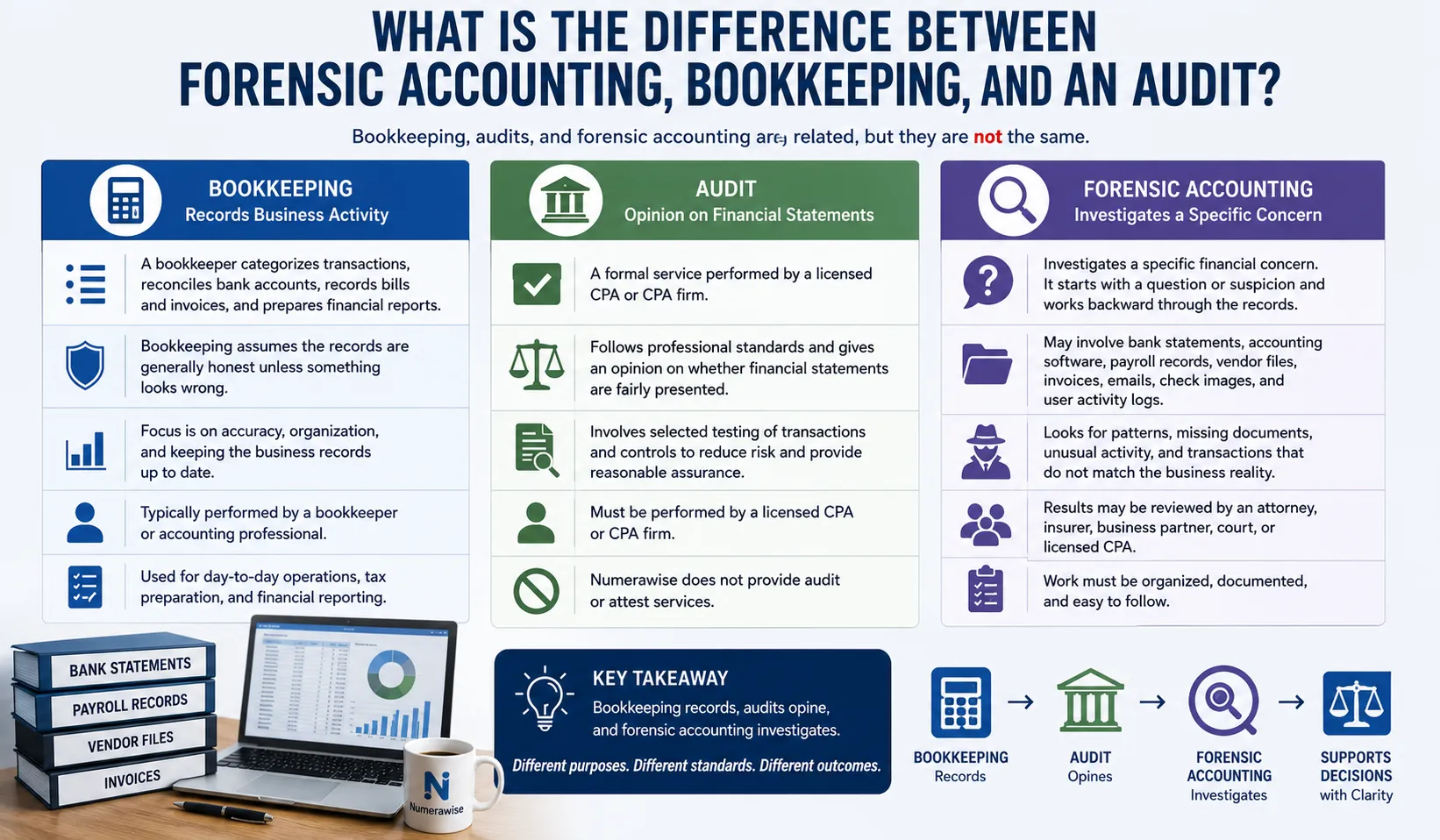

The Difference Between Forensic Accounting, Bookkeeping and an Audit

These three disciplines are related but they serve distinct purposes and carry different professional obligations.

| What to compare | Bookkeeping | Audit | Forensic Accounting |

|---|---|---|---|

| Main purpose | Record daily activity and produce reports | Give an opinion on the financial statements | Investigate a specific concern or suspicion |

| Performed by | Bookkeeper or accounting professional | Licensed CPA or CPA firm only | Forensic bookkeeper, validated by a CPA |

| Starting assumption | Records are generally honest | Independent, standards-based review | Professional skepticism |

| Typical use | Reporting and tax preparation | Assurance for lenders or investors | Fraud, disputes, claims, litigation |

| Does Numerawise offer it? | Yes | No (not an audit or attest firm) | Yes — investigation support |

Bookkeeping

A bookkeeper records the day-to-day financial activity of a business. This includes categorizing transactions, reconciling bank accounts, entering bills and invoices and producing financial reports. Bookkeeping proceeds from the reasonable assumption that the records are generally accurate unless something appears out of place.

Audit

An audit is a formal professional service performed exclusively by a licensed CPA or CPA firm. It follows established professional standards and results in an independent opinion on whether the financial statements are fairly presented. Numerawise does not perform audits or provide any attest services.

Forensic Accounting

Forensic accounting begins with a specific concern or suspicion and works methodically backward through the financial record. It may draw on bank statements, accounting software exports, payroll data, vendor files, invoices, check images and system access logs. Because forensic work is frequently reviewed by attorneys, insurers or courts, the documentation must be thorough, organized and straightforward to follow.

Right time

When Does a Business Need Forensic Accounting?

A business may need forensic accounting support when the ordinary financial reports no longer appear trustworthy. The following situations frequently prompt an engagement:

It is worth noting that not every anomaly reflects deliberate fraud. Some situations stem from poor bookkeeping habits, weak internal controls, aging software or a chaotic system migration. A careful scoping process will distinguish between those possibilities before significant fees are incurred.

Roles & boundaries

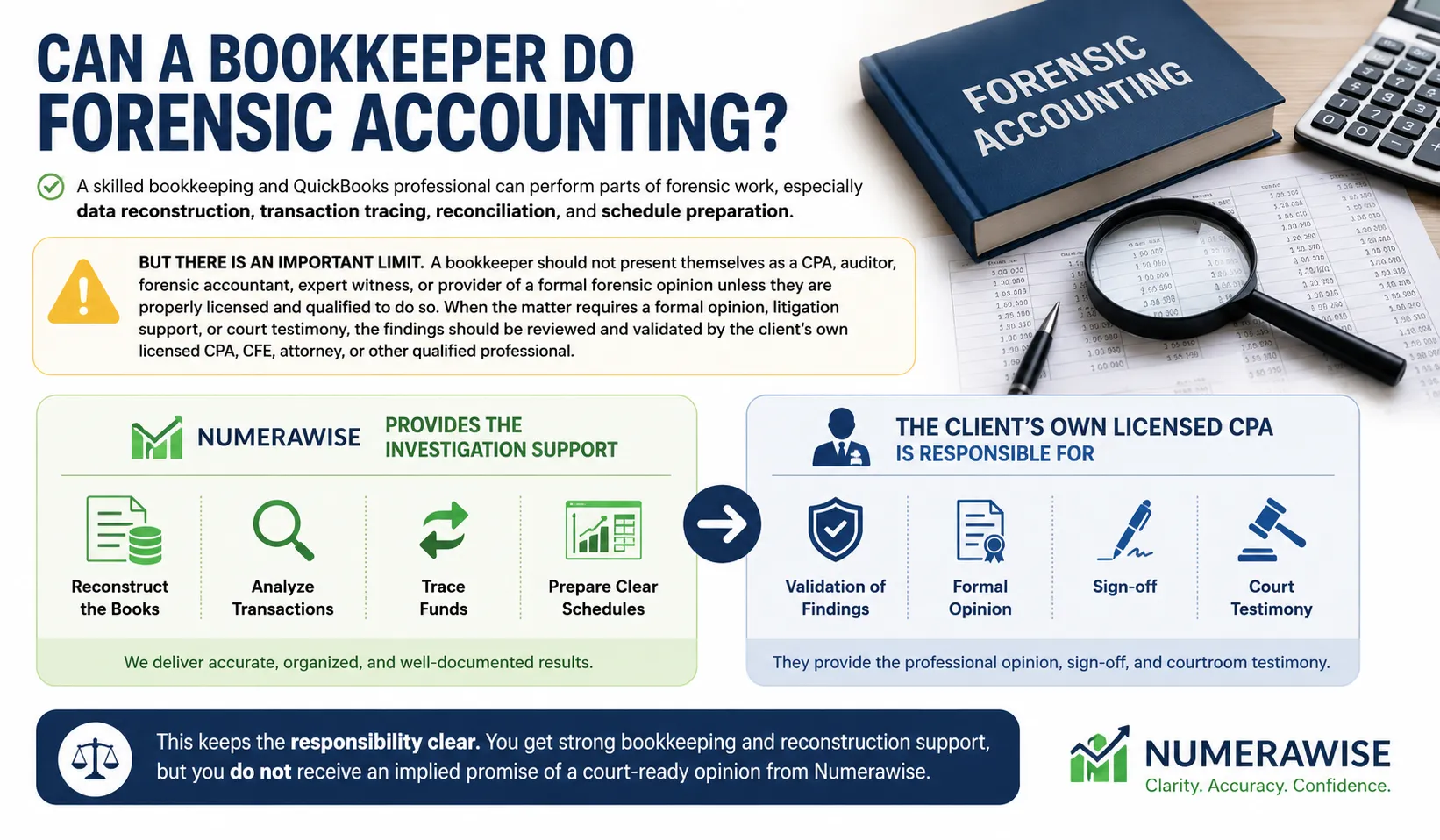

Can a Bookkeeper Perform Forensic Accounting?

A skilled bookkeeping professional can carry out a substantial portion of the investigative groundwork — specifically data reconstruction, transaction tracing, account reconciliation and the preparation of analytical schedules.

There is an important professional boundary, however. A bookkeeper should not represent themselves as a CPA, a forensic accountant, an expert witness or the provider of a formal forensic opinion unless they hold the appropriate license and credentials. When a matter requires a formal professional opinion, litigation support or court testimony, the underlying work must be reviewed and validated by the client’s own licensed CPA, CFE or attorney.

That is the model Numerawise follows. We provide the investigative infrastructure — reconstructed records, traced transactions and clear analytical schedules. The client’s licensed CPA is responsible for validation, formal opinion and any testimony required. This structure keeps professional responsibility exactly where it belongs and ensures the client receives honest, appropriate support at every stage.

Numerawise provides

- Reconstructed records

- Traced transactions and funds

- Account reconciliation

- Clear analytical schedules

Your licensed CPA provides

- Validation of findings

- Formal forensic opinion

- Professional sign-off

- Court testimony, if required

Hands-on data work

What Is Forensic Bookkeeping?

Forensic bookkeeping describes the practical data work that underlies most financial investigations. It focuses on rebuilding and testing the underlying records so that the business owner, attorney or CPA can see precisely what occurred.

A forensic bookkeeping engagement may involve rebuilding QuickBooks from original bank statements, matching recorded deposits against invoices or sales reports, comparing vendor payments to contracts and purchase orders, reviewing owner draws and intercompany transfers, identifying duplicate payments or unexplained journal entries and preparing a chronological transaction timeline with dollar amounts.

For most small businesses this foundational work is the most consequential first step. A CPA or attorney cannot form a defensible position until the underlying data is complete enough to be reviewed with confidence.

A practical example

Suspected Bookkeeper Theft

Consider a small service business whose owner notices persistent cash-flow pressure despite steady sales volume. The bookkeeper attributes the shortfall to slow-paying customers. The owner then receives several emails from those same customers confirming that their payments were submitted weeks earlier.

A forensic bookkeeping review would begin by gathering bank statements, QuickBooks data, customer invoices and deposit records. The analysis would compare what customers paid against what actually reached the bank account, identify any deposits that were recorded in the software but absent from the bank and flag any transfers to unrecognized accounts.

The resulting deliverable would not state that a specific individual committed fraud. That conclusion requires legal and CPA review and is beyond our scope. The deliverable would instead present the documented facts: which customer payments were recorded, which deposits were confirmed by the bank, which transactions lacked supporting documentation and what dollar amount warrants further professional review. The client would then take those schedules to their licensed CPA, attorney or insurer for the appropriate next step.

Investment

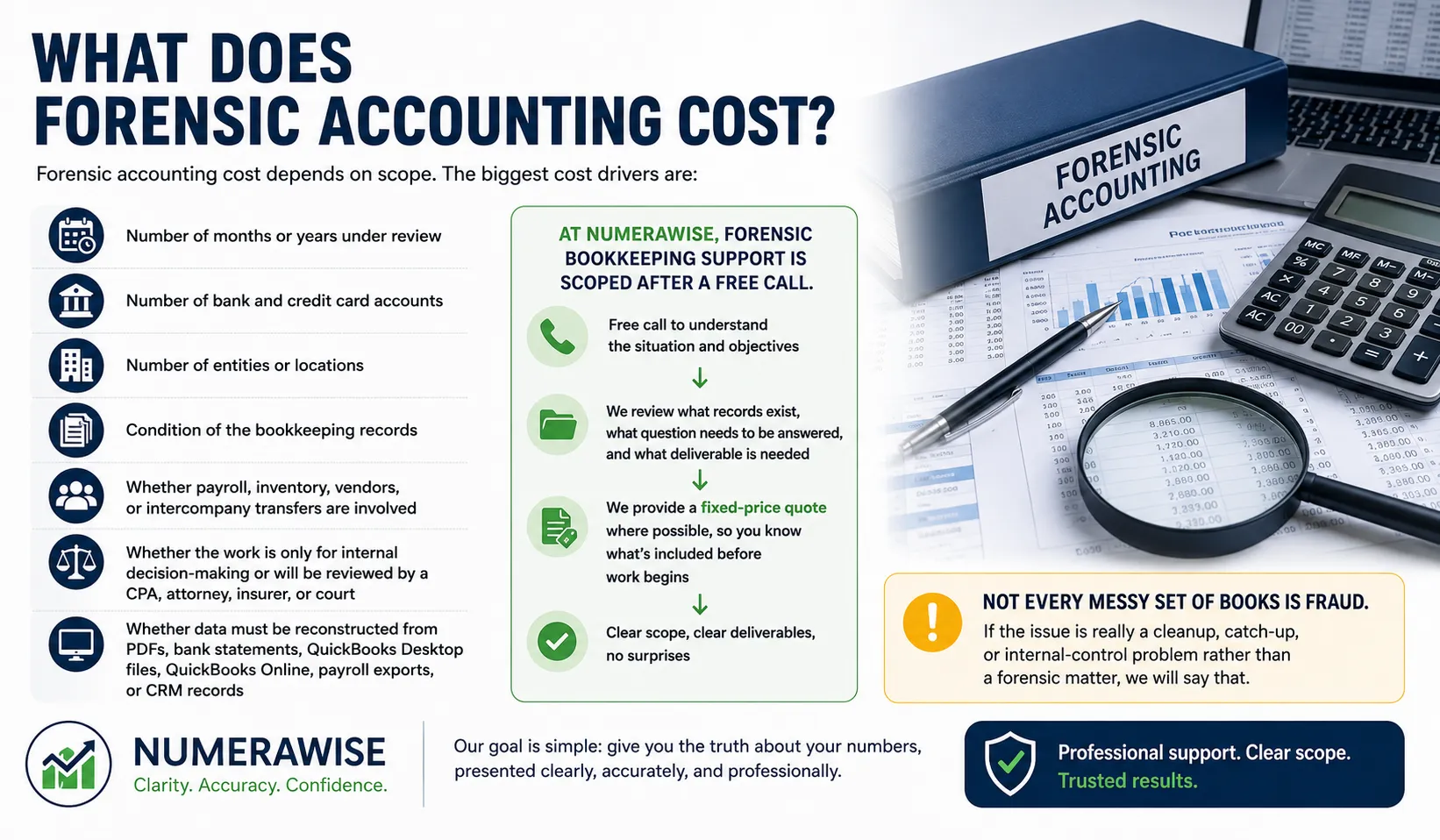

What Does Forensic Accounting Cost?

The cost of a forensic engagement depends almost entirely on its scope. The primary variables include the number of months or years under review, the number of bank and credit card accounts involved, the number of business entities or locations, the condition of the existing bookkeeping records and whether the work is intended for internal decision-making or will be presented to a CPA, an attorney, an insurer or a court.

At Numerawise we scope every engagement through a free introductory call. We review what records exist, define the question that must be answered and determine what deliverable is appropriate. Where possible we then provide a fixed-price proposal so the client understands the full commitment before any work begins.

If the underlying issue turns out to be a cleanup problem or an internal-control gap rather than a genuine forensic matter we will say so directly. Not every disorganized set of books reflects misconduct and the client deserves an honest assessment before spending money on investigative work that may not be necessary.

Our process

How a Numerawise Forensic Bookkeeping Engagement Works

Free Scoping Call

We discuss what you are observing, what records are available and what specific question needs to be answered. This call carries no obligation.

Scope and Fixed-Price Proposal

We define the review period, the accounts to be examined, the software involved, the deliverables and the limits of the engagement. We also make clear at this stage that Numerawise does not provide legal advice, audit services, formal forensic opinions or court testimony.

Data Collection

We collect bank statements, accounting software exports, payroll records, vendor files, invoices, receipts and any other supporting documentation necessary for the analysis.

Reconstruction and Analysis

We rebuild the financial trail, reconcile accounts, trace funds and identify unsupported or unusual transactions. We then prepare clear schedules that document the findings in a form that is straightforward to review.

Findings Package

You receive organized schedules, reconstructed records and a plain-language findings summary. This package is designed to be reviewed by your CPA, attorney, insurer or other qualified advisor.

CPA Validation

Your own licensed CPA is responsible for reviewing and validating our findings, providing any formal professional opinion and handling any testimony that may be required.

Important Engagement Scope

Numerawise provides forensic data reconstruction and analysis only. We do not provide an audit, attest services, legal advice, a formal forensic opinion or court testimony. Validation, formal opinion and any testimony are the client’s responsibility through their own licensed CPA. Clients should confirm with their attorney, CPA and insurance advisor that this service scope is appropriate for their specific matter.

Ready to get the truth about your numbers?

Clarity. Accuracy. Confidence. Let’s start with a free scoping call.

Read more

Explore Our Services

Bookkeeping Support

Accurate, reliable monthly books and reconciliations.

Learn more →QuickBooks Conversion

Clean migrations to QuickBooks from any accounting software.

Learn more →Payroll Support

Organized, well-documented payroll records and review.

Learn more →Talk to Us

Book a free scoping call and get a clear next step.

Contact us →Quick reference

Common Questions

What is forensic accounting?

Forensic accounting is the application of accounting and investigative technique to examine financial records in connection with fraud, disputes, missing funds, insurance claims or legal matters.

What does a forensic accountant do?

A forensic accountant reviews financial records, traces the movement of funds, identifies unusual or unsupported transactions, quantifies apparent losses and prepares findings for review by a CPA, attorney or insurer.

When does a business need forensic accounting?

A business may need forensic accounting when it suspects theft, hidden income, fictitious vendors, misuse of funds by a partner, payroll irregularities, missing deposits or unreliable financial records.

Can a bookkeeper perform forensic accounting?

A skilled bookkeeper can assist with forensic bookkeeping, data reconstruction, reconciliation and transaction analysis. Formal professional opinions, validation and testimony must be provided by the client’s own licensed CPA or other qualified professional.

Does Numerawise testify in court?

No. Numerawise provides forensic bookkeeping support, data reconstruction, analytical schedules and plain-language summaries. Any formal professional opinion or court testimony is the responsibility of the client’s own licensed CPA or qualified professional.

Get a free consultation

Contact Numerawise Solutions

Tell us what you’re seeing. We’ll review what records exist, define the question that needs answering, and give you a clear, honest next step — with no obligation.